Quarterly Tax Instalments in Canada 2026 — Self-Employed Guide

Miss a single quarterly instalment payment and the CRA starts charging interest immediately — at a prescribed rate that currently sits around 10% annually, compounded daily. For self-employed Canadians, understanding the instalment system isn't optional. It's the difference between a smooth tax season and an ugly surprise.

Understanding the Instalment System

The Canada Revenue Agency doesn't wait until next April to collect the taxes you owe. Instead, they require self-employed people to submit quarterly tax instalments spread throughout the year — essentially pre-paying their expected tax liability in four equal chunks.

This system exists because the CRA wants steady cash flow, and because self-employed Canadians can't rely on employer withholding. But for many people, the instalment system feels like an invisible tax burden nobody explained clearly.

By the end of this guide, you'll understand exactly when instalments are due, how to calculate them, and most importantly, how to avoid the penalties and interest that catch so many self-employed people off guard.

Do You Need to Pay Instalments?

Not every self-employed person has to pay quarterly instalments. The CRA has a specific threshold:

You must pay instalments if you owe more than $3,000 in net tax in each of two consecutive years.

In Quebec, the threshold is lower: $1,800.

Here's how the CRA determines if you're subject to instalments:

- Year 1: You file your tax return and owe $3,500 in net tax (after credits). You're now flagged.

- Year 2: You file your tax return and owe $3,200 in net tax. Because you've met the threshold for two consecutive years, you're required to pay instalments for Year 3.

- Ongoing: Once you're in the instalment system, you stay there unless you drop below the threshold in a given year.

The CRA notifies you when you've crossed the threshold, usually in your notice of assessment. But don't wait for the letter — if you know you're going to owe more than $3,000, start planning instalments now.

Pro Tip: Check Your Status

Log into CRA My Account to see whether the CRA believes you're required to pay instalments. It's not always obvious, and the CRA's records sometimes lag behind reality. If you disagree with their assessment, you can appeal.

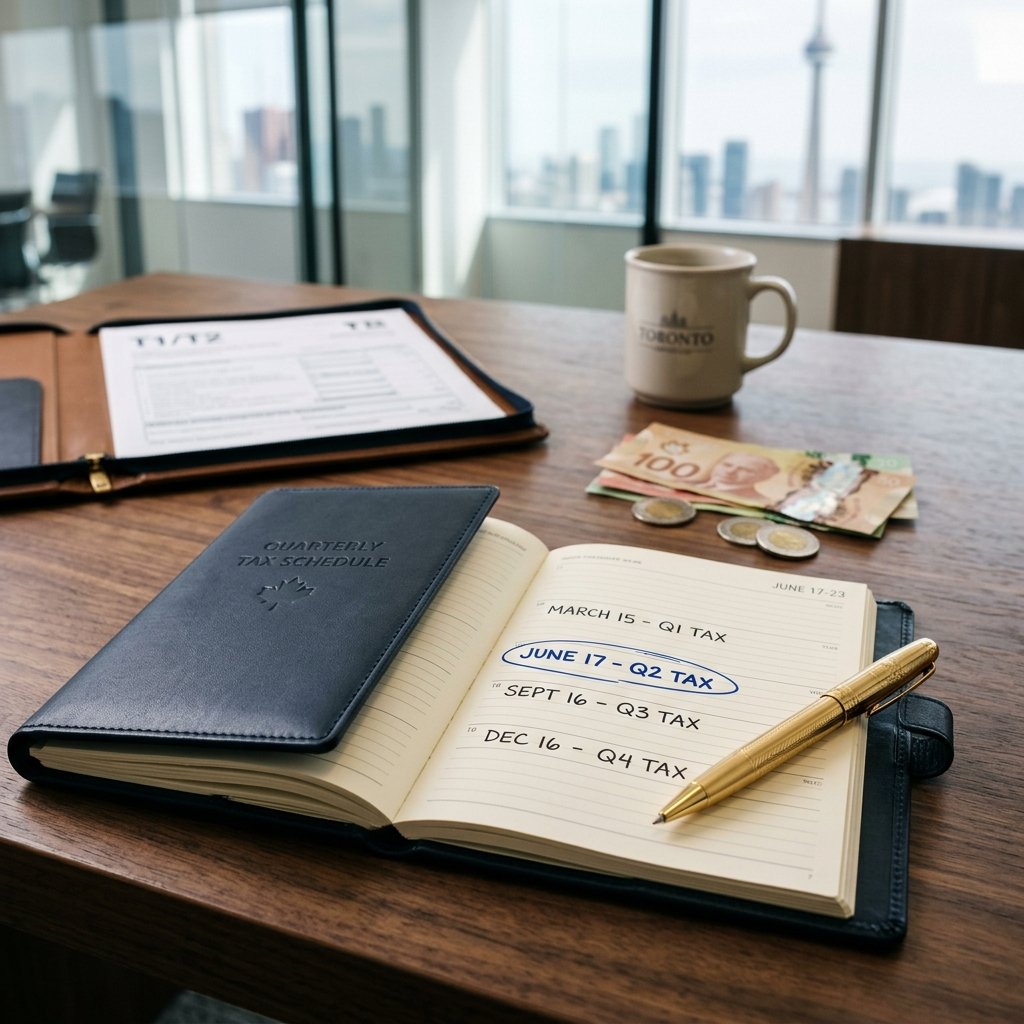

2026 Instalment Due Dates

For 2026, the CRA has set four quarterly instalment due dates. Mark these on your calendar and set reminders — the CRA won't send you a bill, and they start charging interest the day after the due date if you miss it.

| Quarter | Due Date | Notes |

|---|---|---|

| Q1 | March 15, 2026 | First instalment of the year |

| Q2 | June 15, 2026 | Same date as your tax filing deadline |

| Q3 | September 15, 2026 | Third instalment |

| Q4 | December 15, 2026 | Final instalment of the year |

You can pay online through CRA My Account, by phone, by bank transfer, or by mail. Online is fastest and leaves no room for postal delays.

The Three Calculation Methods

The CRA gives you three options for calculating your quarterly instalment amounts. Each has pros and cons depending on your income situation.

Method 1: Current-Year Method

Calculate your estimated tax liability for 2026, then divide it by 4.

Best for: People whose income is relatively stable or growing predictably.

Example: You expect to earn $100,000 in net self-employed income in 2026. Your marginal tax rate is 50%, so your estimated tax liability is $50,000. Divide by 4 = $12,500 per quarter.

Risk: If you underestimate your income, you'll owe a larger balance at tax time. If you overestimate, you'll get a refund (but you've tied up cash unnecessarily).

Method 2: Prior-Year Method

Use your actual tax liability from 2025, divide it by 4, and pay that amount all year.

Best for: People whose income is uncertain or volatile. Also good if you want the simplest calculation possible.

Example: You owed $20,000 in net tax in 2025. Your 2026 instalments are $5,000 per quarter, regardless of what you actually earn in 2026.

Advantage: You're protected. If your 2026 income drops, you've overpaid and you'll get a refund. If your income shoots up, you'll owe a balance at tax time, but no penalty.

Risk: If your income falls significantly, you're tying up more cash than necessary.

Method 3: CRA Suggestion Method

The CRA sends you a suggested instalment amount, typically based on a blend of your current-year and prior-year tax liabilities. This is what many people do because it takes the guesswork out.

Best for: Anyone who wants to minimize the risk of penalties while staying compliant.

How it works: The CRA calculates a reasonable amount based on your recent history and mails it to you (or makes it available in CRA My Account). You can use their suggestion, or calculate your own using Methods 1 or 2.

Why it matters: If you use the CRA's suggestion and your instalment interest exceeds $1,000, you're protected from the additional penalty (more on that below).

| Method | Calculation | Best If... | Risk |

|---|---|---|---|

| Current-Year | Estimate 2026 tax ÷ 4 | Income is stable or growing | Underestimation leads to larger balance owing |

| Prior-Year | 2025 actual tax ÷ 4 | Income is uncertain or volatile | Overpayment ties up cash |

| CRA Suggestion | CRA blends methods | You want simplicity and protection | May not match your actual liability |

How to Choose

Most self-employed people choose either the CRA Suggestion Method (for simplicity) or the Prior-Year Method (for flexibility). The Current-Year Method requires more accurate income forecasting and is riskier if you're wrong.

What Happens If You're Late or Short

This is where the consequences get real. The CRA takes instalment compliance seriously.

Interest on Late Payments

If you miss a due date, the CRA charges interest on the shortfall from the due date forward. The prescribed interest rate is approximately 10% annually, compounded daily (as of late 2025).

Example: Interest Calculation

Scenario: Your Q2 instalment (due June 15) is $5,000, but you only pay $3,000. You don't pay the remaining $2,000 until September 15.

Shortfall: $2,000

Period: June 15 to September 15 = 92 days

Interest rate: 10% annually = ~0.0274% per day

Interest owed: $2,000 × 0.10 × (92/365) = ~$50.41

This is in addition to the $2,000 principal you still owe.

The Penalty Threshold

Here's where it gets harsher: if your total instalment interest exceeds $1,000 in a year, the CRA adds a penalty of 50% of the interest above the greater of $1,000 or 25% of the interest you would have owed if you'd made no instalments.

That sounds complicated. Here's what it means in practice:

Example: Penalty Calculation

Scenario: You made all your 2026 instalments, but they were all short by $1,000 each. Your total instalment interest comes to $1,500.

Interest owed: $1,500

Threshold: $1,000

Amount subject to penalty: $1,500 - $1,000 = $500

Penalty (50% of $500): $250

Total cost: $1,500 (interest) + $250 (penalty) = $1,750

Protection: The CRA Suggestion Method

If you use the CRA's suggested instalment amounts and your interest still exceeds $1,000, you're typically protected from this penalty. This is another reason why many people choose the CRA Suggestion Method.

The Cash Flow Strategy: Setting Aside Money for Instalments

The biggest mistake self-employed people make is spending their tax liability as it comes in. One day you invoice a client for $10,000, and by next week it's been spent on supplies, payroll, or reinvestment. Then Q2 rolls around and you don't have $5,000 for instalments.

The solution is simple but discipline-intensive: set aside 25-30% of every invoice or payment into a separate, dedicated account.

How to Implement a Cash Flow System

- Open a high-interest savings account (HISA) specifically for tax instalments. Don't mix it with operating cash.

- Calculate your effective tax rate. If you expect to earn $100,000 and owe $30,000 in tax, your rate is 30%. Round up to 33-35% to create a buffer.

- Move money weekly or bi-weekly from your operating account to your tax account based on invoices paid or revenue received.

- Track your balance monthly. You should know exactly where you stand relative to upcoming instalments.

- Reinvest or earn interest on the money sitting in your tax account. A high-interest savings account earning 4-5% helps offset some of the cost of saving.

Cash Flow Example

Your situation: You expect $120,000 in net income and $36,000 in tax (30% rate). Your quarterly instalment is $9,000.

Monthly cash flow: You invoice clients $10,000/month on average.

Each month: Move $3,000 to your tax account (10% of revenue). This builds to $9,000 by the time the first quarterly instalment is due (March 15).

The benefit: By Q4, you've already paid your entire annual tax liability. Tax time in April is stress-free.

Monthly Tracking Template

Create a simple spreadsheet with columns: Date, Invoice Amount, Tax Amount Set Aside (30%), Running Balance, Upcoming Instalment Due. Check it every month. This one habit prevents most instalment problems.

The April 30 Trap: A Deadline You Can't Ignore

Here's the trick that catches many self-employed people: Your tax filing deadline is June 15, 2026, but any balance owing must be paid by April 30, 2026.

This creates a three-week window where you owe money, but you haven't filed yet.

Critical Timing Issue

You must estimate your full 2026 tax liability by April 30 and pay any amount owing. If you wait until June 15 to file and discover you owe money, interest has been accruing since May 1. The prescribed interest rate is approximately 10% per year, so every month of delay costs you about 0.83% on top of your tax bill.

Here's why this matters:

- You can't file early with the CRA (they process returns in order, mostly). But you can calculate your own estimated liability.

- If you've made all four quarterly instalments, you might have already paid your full liability. Check the math early.

- If you owe more than your instalments covered, April 30 is when the CRA expects payment, not June 15.

- Interest on unpaid tax starts May 1. Not June 15. Not July 1. May 1.

Best Practice: Project Early

In late March or early April, estimate your total 2026 tax liability. Subtract the instalments you've already paid. If there's a balance, pay it by April 30 to avoid interest. You can file your full return later with no penalty, even if you've overpaid.

Quick Tips for Managing Instalments

1. Automate Your Transfers

Set up automatic transfers from your operating account to your tax savings account every Friday or every 15th and last day of the month. Automation removes emotion and prevents the "I'll do it later" trap.

2. Use CRA My Account to Check Suggested Amounts

Log into CRA My Account quarterly and check what the CRA thinks you should be paying. If their suggestion differs from your calculation, investigate why. The CRA might have updated information or there might be a discrepancy in their records.

3. Adjust Mid-Year If Your Income Changes Significantly

If you expected $100,000 in income but by July it's clear you'll only earn $60,000, contact the CRA and request a reduction in your remaining instalments. The CRA is surprisingly flexible here if you ask in writing and explain the change.

4. Pay Online or By Bank Transfer

Never mail a cheque. Online payments are processed immediately, and you get a confirmation number. Mailed cheques can take weeks to process, and the CRA counts the due date, not the day they receive it.

5. Keep Detailed Records

Save confirmation numbers, bank statements, and CRA correspondence. If the CRA ever disputes whether you paid an instalment, you'll have proof.

6. Don't Assume Instalments Are Tax Payments

Instalments reduce what you owe at tax time, but they're not the same as filing your tax return. You still need to file by June 15 and reconcile your actual income with the instalments you paid.

Final Thoughts

Quarterly tax instalments are one of those areas where self-employed Canadians can get blindsided if they don't plan. But the system itself isn't complicated once you understand it:

- If you owe more than $3,000 in tax, you're likely required to pay instalments.

- Instalments are due March 15, June 15, September 15, and December 15.

- You have three calculation methods; pick the one that fits your income situation.

- Interest and penalties are harsh, but preventable with good cash management.

- April 30 is the real deadline for paying 2026 tax; don't wait until June 15.

The best time to get serious about instalments is right now, before Q2 is due. Set up a dedicated savings account, calculate your likely quarterly payment, and commit to paying on time. Your future self will thank you when tax season arrives and there are no surprises.

Get the Complete Self-Employed Tax Checklist

Download our free ebook for self-employed Canadians. It covers instalments, expense deductions, GST/HST obligations, and the April 30 deadline — everything you need to file with confidence.

Explore Canadian Optimizer →

Andrew Carrothers

Strategy Lead & Founder

Andrew is a financial strategist dedicated to helping Canadians optimize every dollar. With over 15 years of experience in personal finance and portfolio optimization, he focuses on tactical wealth building.

Master Your Financial Optimization

Join 5,000+ Canadians receiving our weekly "Optimization Tactics" directly to their inbox. Get our free 5-day starter guide instantly.

No generic tips. No spam. Only optimization tactics.